A new study from Angi examined different home renovations that pay off by boosting your property value. (iStock)

Home renovations can add value to your home while also making it a better place to live, and some improvements are more likely to pay off when it comes time to sell. A recent study from Angi (formerly Angie’s List) shared what it said are the top home features that boost a property’s value, from intricate feature updates to extensive home improvement projects.

“Spruce up your home with your dream features, and you could boost its eventual sale value by more than the features cost,” the article said.

The most value-boosting feature across all U.S. housing markets was the pot filler, a kitchen sink attachment located over your cooktop that makes it easier to add water while cooking. Angi estimated that installing this fixture could cost between $600 to $2,000 — but that it pays off with a 3.20{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9} price premium.

Other features coveted by today’s homebuyers that pay off in higher property values include:

- Pendant lighting (2.66{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Under cabinet lighting (2.48{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- His-and-hers sinks (2.35{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Barn doors (2.32{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Butcher block (2.26{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Quartz countertops (2.26{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Oversized windows (2.23{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Farmhouse sink (2.22{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

- Subway tile (2.13{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9})

REFINANCING FOR HOME REPAIRS AND IMPROVEMENTS: HOW DOES IT WORK?

The most value-boosting improvement also depends on where you live. For example, Angi said that homeowners in the New York area have the most to gain by installing a garage (18.47{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9}) — a coveted feature in a market where off-street parking comes at a premium. In San Francisco, known for its year-round sunny climate, sellers can add the most value to their homes by adding a pool (11.35{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9}).

While some of these property features are relatively cheap to purchase and install, others require a sizable upfront investment. For example, adding a garage to your home costs an average of $27,500, according to HomeAdvisor by Angi, while building a pool will cost you about $32,000 on average.

Fortunately, there are several ways to finance renovations that allow homeowners to tap into their existing home equity or break their upfront costs into fixed monthly installments. Keep reading to learn more about home improvement financing, and visit Credible to compare rates on borrowing products like unsecured home improvement loans and cash-out mortgage refinancing.

THINKING OF REFINANCING YOUR MORTGAGE? HERE’S THE MINIMUM CREDIT SCORE YOU’LL NEED

3 ways to finance home improvements

A recent study said that the average American homeowner can gain nearly $200,000 in value by remodeling, but many consumers could be held back by the steep upfront cost of home renovations. Thankfully, there are several ways to finance home improvement projects, including:

Read more about each strategy in the sections below.

1. Cash-out mortgage refinancing

Mortgage refinancing is when you take out a new home loan with better terms to pay off your existing mortgage. Cash-out refinancing is when you borrow a mortgage that’s larger than your current home loan, effectively allowing you to pocket your home’s equity in cash which you can use to pay for home improvements.

The average homeowner gained more than $55,000 in home equity in 2021, according to a new report, which gives some borrowers the opportunity to access more money than ever with a cash-out refinance.

Keep in mind that mortgage refinancing comes with closing costs, which are typically between 2{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9} and 5{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9} of the total loan amount. Plus, mortgage rates have surged quickly in 2022, which means it’s important to shop around for the lowest rate possible for your financial situation.

You can visit Credible to compare mortgage refinance rates across multiple lenders at once. That way, you can rest assured that you’re getting a competitive rate while financing home renovations.

HOW TO AVOID A MORTGAGE PREPAYMENT PENALTY

2. Home equity loans and HELOCs

Another popular home improvement financing option is a home equity loan or home equity line of credit (HELOC). This is a separate loan in addition to your first mortgage that lets you borrow against the equity you’ve built in your home.

While home equity loans come with a fixed loan amount and repayment terms, HELOCs allow you to borrow just what you need from a revolving credit line. Both borrowing options are secured loans that use your home as collateral, which means the creditor can seize your property if you fail to repay the loan.

Most home equity loan and HELOC lenders let you borrow up to 85{d4d1dfc03659490934346f23c59135b993ced5bc8cc26281e129c43fe68630c9} of your home’s appraised value. Like with cash-out mortgage refinancing, these types of loans require the borrower to pay closing costs.

You can learn more about calculating your home equity on Credible.

PERSONAL LOAN ORIGINATION FEES: ARE THEY WORTH THE COST?

3. Unsecured personal loans

Unlike other secured loan options for home improvement financing, personal loans are unsecured and don’t require you to use your home as collateral. They allow you to borrow a lump-sum of cash that you repay at a fixed interest rate in predictable monthly payments over a set repayment period, typically a few years.

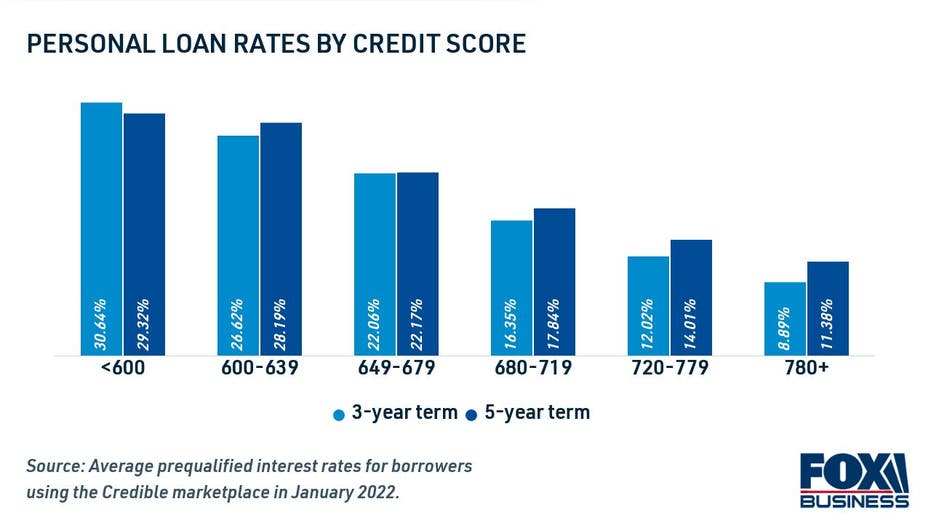

Since personal loans are unsecured, lenders determine eligibility and loan terms based on a borrower’s credit history. Applicants with good credit and a low debt-to-income ratio (DTI) will qualify for the lowest rates available, while those with fair or bad credit may see higher rates — if they qualify at all.

GETTING A SECOND MORTGAGE? HERE’S WHAT YOU NEED TO KNOW

Another benefit to using a personal loan for home improvement is that lenders offer fast funding. The loan amount may be deposited directly into your bank account as soon as the next business day after loan approval. This is in contrast to home equity options, which require a longer closing period. Plus, short-term personal loan rates are currently near historic lows, according to data from Credible.

You can browse current personal loan interest rates in the table below. And you can visit Credible to get prequalified through multiple online lenders at once for free without impacting your credit score.

VETERANS BORROWING VA LOANS AT A RECORD PACE, STUDY SHOWS

Have a finance-related question, but don’t know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.